This article examines the long-term cycles of technological innovation, financial crises, and economic growth over the past two centuries. It summarizes key research on the periodic surges of breakthrough innovations, their relationship to major financial downturns, and the resulting fluctuations in productivity and output.

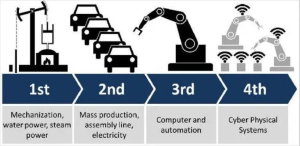

The analysis draws on data going back to the early 19th century to identify four distinct industrial revolutions driven by general purpose technologies like steam engines, electricity, automobiles, and information technology. Each revolution has followed a similar cycle marked by an initial installation phase with limited applications, a frenzy of investment and overheating, a major financial crash, and finally a deployment phase with full diffusion of the technology.

Looking at the first surge in the Age of Steam and Railways beginning in the 1830s, both the United States and United Kingdom experienced robust growth during the installation period. However, a crisis in 1848-1850 preceded an even stronger expansion from 1850-1873 as steam power was deployed across industries. The same pattern recurred in the second revolution from 1875-1918 based around steel, electricity, and heavy engineering. Growth was solid in the installation years up to 1893, but really took off after a panic in 1893-1895 led to a broader application of electrical power and industrial motors.

The more recent cycles follow the same sequence but with a weaker rebound after financial crises. In the Age of Oil, Automobiles and Mass Production beginning in 1908, the deployment phase from 1929-1943 brought only a modest recovery from the Great Depression. And the current Information and Telecommunications revolution launched in 1971 has seen GDP growth slow to just 1.5 percent per year since 2010 despite a massive burst of innovation in Silicon Valley.

Understanding this cycle of technological development can help explain the surges and slowdowns in productivity growth over the past century. As the research cited here shows, breakthrough innovations tend to arrive in clusters driven by non-rival ideas and increasing returns to scale. But it takes a broader financial reckoning and institutional restructuring before the full benefits are realized.

Looking at the quality of patent innovation using modern data techniques, the upward spikes in impactful patents align closely with the start of each industrial revolution. Moreover, aggregate productivity jumps about 2 percentage points in the 5-10 years after bursts of high quality patent activity. The problem is that much of the economy remains stuck in older technologies and management habits, resulting in a crisis that forces adaptation.

The data on capital investment illuminates this cycle. Capital deepening accelerates in the deployment phase as outdated facilities are replaced. But it then slows dramatically for decades as long-lived equipment continues providing productive services. This makes the installed base of capital a hindrance to absorbing new technologies, until enough of it retires to necessitate modernization.

The aging of America’s capital stock can be seen in the period of weak investment between 1930 and 1945. With fewer new assets added, the average age of fixed business capital rose from 15 to 20 years. It took the postwar boom of the 1950s and 1960s to bring this back down. But then aging resumed, with the average age now back near 1920s levels. The result is an innovation gap, where breakthroughs happen but their productivity benefits build only slowly.

Bridging this gap requires more than just scientific creativity. It involves financial and organizational reengineering to remove incumbent resistance and channel funding to new firms and industries. This was achieved after past crises through tight money, bankruptcies, and greater income equality. But so far policy has avoided this “creative destruction,” leaving economies stuck in a post-crisis malaise.

The lesson is that major technological revolutions reshape societies as well as companies. Realizing their full benefits depends on social readiness as much as the raw potential of the technology. This suggests greater attention to financial regulation, labor markets, and education so that innovative ideas can be absorbed and propagated. With the right institutional conditions, surges of creativity can translate into broadly shared gains instead of crises and stagnation.